Are Small Business Loans Access In Jeopardy?

Are Small Business Loans Access In Jeopardy?

Are Small Business Loans Access In Jeopardy?

While many experts are predicting a mild recession either late this year or early next year, there are also some troubling signs popping up. Small businesses tend to be more focused on retail customers than businesses as a whole. And until recently, consumers were in relatively good shape, buoyed by covid payments from the federal government and high overall employment rates. But inflation is taking its toll. Savings rates are on a big decline. More troubling, automobile loan defaults are rising while used car prices are declining from their recent lofty levels. Some are predicting a decline of as much as 20% in used car prices within the next twelve months.

A story in The Playbook by senior reporter Andy Medici, the failure of Silicon Valley Bank and two other mid-sized banks has banks seeing more scrutiny from federal regulators. The likely result is that all banks will become more cautious to protect their balance sheets. We are seeing some data that specifically looks at patterns of loan approvals to small businesses, and the trend is not positive in North Carolina.

Alarmingly, this trend actually began in 2018. While the low was in 2020 during covid, we are again seeing a downward movement that began 10 months ago. According to the Biz2Credit Small Business Lending Index, loan approval rates declined for 11 straight months through April, the last month available. According to Rohit Arora, CEO of Biz2Credit, there is a real danger that small businesses are about to experience a credit crunch.

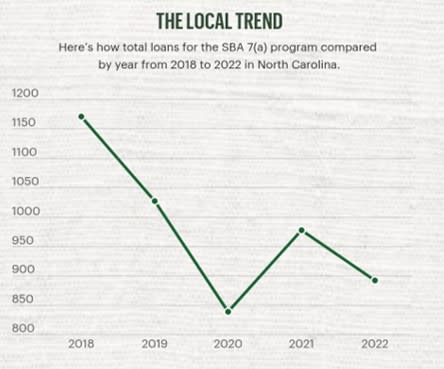

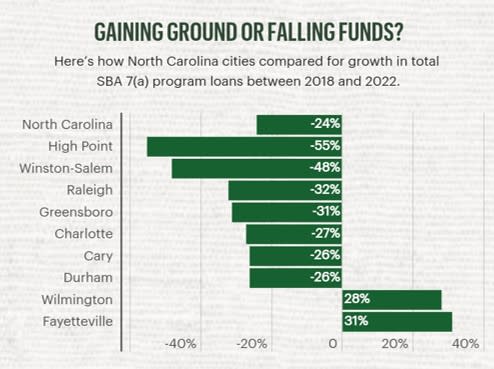

In North Carolina, the total SBA loans granted followed this trend. According to SBA data, between 2018 and 2022 overall loans in North Carolina are down 22%.

As interest rates rise, payments rise. For existing bonds, the underlying value of the asset goes down. All this means that banks have to generate higher returns on loans in order to generate a positive return on investment. This can sometimes result in banks demanding new terms and conditions that small businesses haven’t seen before, and may be onerous. It is more important than ever for small businesses to scrutinize loan documents and understand all the terms and conditions before signing.

Meanwhile, the Small Business Administration is being criticized for outdated methods which result in long delays on SBA backed loans. Multiple investment organizations have released suggestions on how the SBA should modernize and streamline the loans approval process.

The bottom line is if you are a small business looking to need capital here are some recommendations:

- Start the process very early. Give yourself a minimum of six months

- Make sure your financial records are complete and your loan purpose is detailed

- Once you receive documents, review them in detail for new terms and conditions

- Be prepared for multiple delays and even times when you have to submit the same information multiple times

Even if you do not need a loan now, keep aware of lending trends. They may be one valuable sign of market sentiment as a whole.